Underneath the education loan-old age matching system, businesses can fits efforts, as much as a particular payment, whenever a member of staff tends to make a qualifying education loan percentage to their employer-sponsored 401(k), 403(b), 457, otherwise Effortless IRA account.

In lieu of deposit a fraction of your salary on your own 401(k) so you’re able to max your manager suits – generally earning your totally free currency – you get a similar boss match work for after you create a great qualifying mortgage payment. A matching share the most powerful old-age discounts masters for gurus to expand a lot of time-long-term riches.

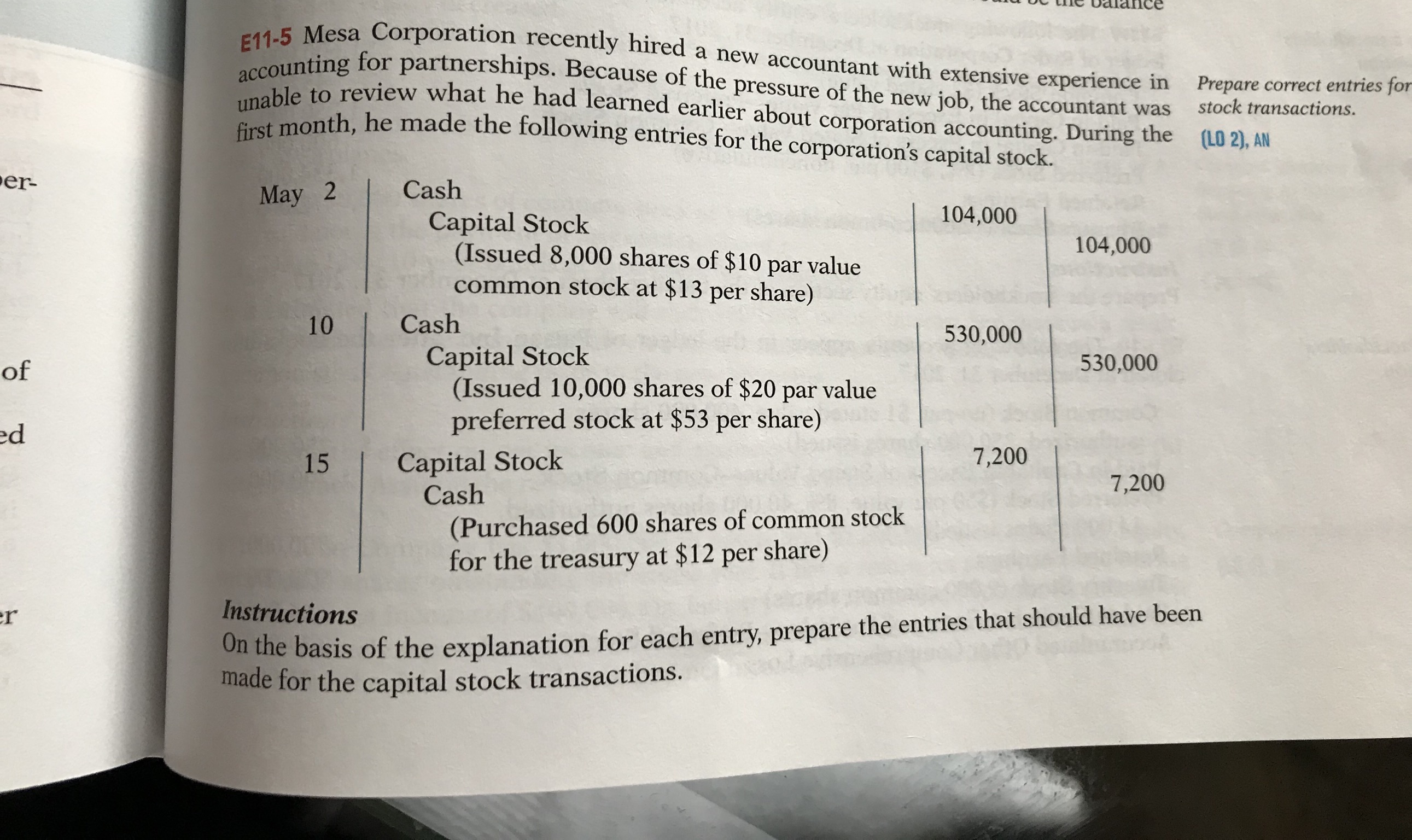

Think of, 401(k) education loan matches must comply with an equivalent fits percentage, eligibility, and you will vesting legislation just like the salary deferrals.

People boss providing qualifying agreements can provide a good 401(k) education loan matches as a worker benefit. If curious, believe contacting their employer’s Hour to share with them with the this new chance. It can be as easy as sending a contact.

Alleviates financial stress on group

Of a lot U.S. personnel be unable to repay the student loan debt, tend to failing to contribute continuously on their office old-age plans and you will compromising the extra benefit of boss-coordinating benefits. From the forgoing its 401(k) or other plans, professionals including miss out on numerous years of taxation-deferred otherwise taxation-free progress.

The newest Safe Work 2.0 alleviates certain teams with the financial filter systems by allowing all of them to make 100 % free old age currency when they make being qualified student loan repayments.

“Getting rid of student loan financial obligation will benefit the latest economy by moving forward household resources out-of personal debt installment so you can investment and you will expenses, also improved private returns,” teaches you Greenip.

Helps employers focus and you will preserve talent

A pension plan instance an excellent 401(k) otherwise retirement is one of the way more notable professionals will found of the experts. not all the offices provide employer-complimentary benefits, companies that would generally have a less complicated day attracting and you may preserving gifted employees.

An excellent 401(k) match chance for salary deferrals and you will qualifying education loan money appeals so you’re able to You.S. experts looking to get the best of each other globes. Additionally, staff tends to be significantly more motivated to stand through to the financing when you look at the the senior years bundle are completely vested (three to five many years).

Irs great tips on 401(k) education loan suits system

Initially, this new Irs offered nothing information the application form, as well as what was sensed a great “qualifying” education loan fee and exactly how employers was likely to track and you loans Hayward can authorize its employees’ education loan efforts.

“Staff member deferrals so you’re able to retirement agreements try given from the employers by themselves, it is therefore relatively simple to trace benefits,” Greenip explains. “While the businesses do not tune student loan costs, so it adds a sheet of difficulty and you will management support that will be needed to own work for.”

On the August 19, the newest Internal revenue service provided interim information 401(k) student loan fits, particularly on the Part 110 of your own Secure dos.0 Work.

Whom qualifies to possess a good 401(k) student loan suits?

- Old-age preparations that be eligible for a student-based loan fits try 401(k)s, 403(b)s, Easy IRAs, and you may regulators 457(b)s.

- This new Internal revenue service defines licensed education loan money (QSLPs) once the repayments produced by a member of staff to a being qualified student loan of the worker, the newest employee’s lover, or a depending. The fresh new personnel also needs to feel legitimately forced to generate student loan payments.

- Education loan cosigners aren’t the main borrowers. For this reason, they are certainly not entitled to a 401(k) student loan fits.

- The group just who be considered for regular boss-sponsored matches qualify to own education loan matches. Brand new regularity from complimentary contributions can vary of normal manager-meets benefits but should be one or more times a year.

Advice to own old-age plan providers

- Financing costs produced by a member of staff amount into the fresh new yearly limitation to your optional deferrals.

- Advancing years package company usually do not is conditions that limitation student loan suits to simply certain kinds of education funds. Most of the workers are permitted discover complimentary efforts with the being qualified college student mortgage costs regardless of loan method of, attendance during the a specific university, or a particular studies system. not, a strategy consist of have simply relevant to help you low-together bargained employees.